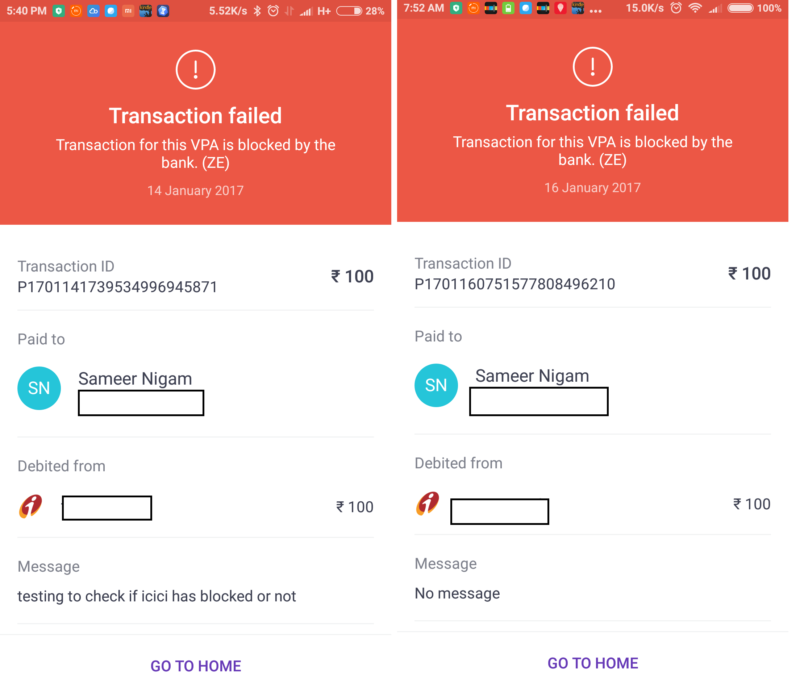

We've updated two points below, following clarifications Why should you build for UPI if individual banks can stop their users from accessing your application, by shutting off the apps bank account? It has been almost four days since ICICI Bank blocked its customers from using PhonePe, the Unified Payments Interface service from Yes Bank, which is managed by Flipkart owned PhonePe. PhonePe founder Sameer Nigam pointed this out on Twitter, saying, that "@ICICIBank is blocking all @ybl & @PhonePe_ txns since Friday. No intimation. No provocation. Not cool at all!" I tried, and as an ICICI Bank customer, I couldn't send money via UPI using the PhonePe app. @ybl is the Yes Bank Virtual Payment Address (VPA) address that is created for UPI users on PhonePe, given that PhonePe is essentially a YesBank application run by PhonePe. In the same way, the State Bank of India hasn't allowed netbanking transfers to wallets for quite a while now; the payments industry is entirely dependent on the opinion of banks, not on principles or policies set by a regulator. MediaNama readers should note that ICICI pulled the plug on PhonePe the same day that Flipkart became a merchant on UPI. ICICI Bank's response and issues with it In response, ICICI Bank issued a statement to Mint, with the following key points: 1. Security issues with data: ICICI Bank says "Some banks including us have raised security related concerns at appropriate forums about the access to UPI data to a non-banking application” MediaNama's take: Firstly, payments is…