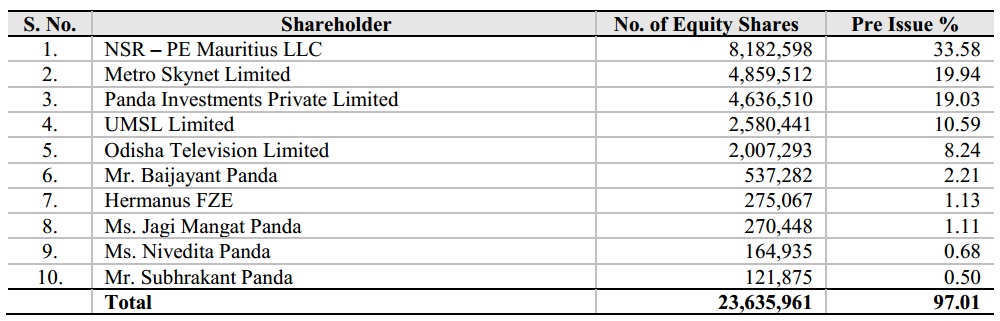

by Nikhil Pahwa and Shashidar KJ Ortel, an Odisha-based cable and broadband provider, is looking to raise Rs 217.2- 240 crore through its initial public offering (IPO) by issuing up to 12 million equity shares of face value Rs 10 each. The price band is fixed from Rs 181 to Rs 200 per equity share. Ortel is a regional cable and broadband provider focused in the states of Odisha, Chhattisgarh, West Bengal and Andhra Pradesh. It currently offers services in 48 towns and certain adjacent semi-urban and rural areas with over 21, 600 kms of cables and supported by 34 analog-heads and five digital head-ends. The Last Mile Pitch In the RHP, Ortel makes a very strong pitch of its ownership of the last mile as being a competitive advantage. It says that in comparison, in a franchise model, the Local Cable Operators can shift from one MSO to another, causing large scale customer churn. Control in a 'last mile' model like Ortel's, it says, reduces risk of a large scale loss and helps in stable business operations. Apart from this, it enables the company to collect subscription revenues directly from customers, cross selling services and increasing revenues per user. As on March 31, 2014 88.02% of Ortel's cable subscriber base is on their own ‘last mile’ network and the remaining is connected through LCOs. Ortel acquired this last mile by entering into agreements with 486 Multiple System Operator (MSO) / Local Cable Operators (LCOs) between April 1, 2009 and June 30, 2014, resulting in an acquisition of 212,980 cable television subscribers. As a…